End of the Golden Visa

DÉJÀ VU…

THE END OF THE PORTUGUESE GOLDEN VISA…again?

It feels like ground hog day (or week) writing this…

In September of 2022, I penned a 3-part article that can be found here: The changing portuguese real estate market ( Part 3 ) – ALL ABOUT RETIREMENT OVERSEAS, analysing the factors that had contributed to the change in the real estate landscape. I also pointed out the need for structural change in Portugal’s development landscape to allow for more, and more affordable, product, to make its way to the market.

In November 2022, in an article that can be found here: The End of the Portuguese Golden Visa?, I referenced the Portuguese Prime Minister’s comments at the 2023 Web Summit. António Costa threw the cat among the pigeons by stating the Golden Visa program probably did not justify being retained.

The ensuing debate was emotive and every participant (including yours truly) had an opinion. As I have repeated many times, any statement by a senior Portuguese figure is usually a precursor to action. A proposal may undergo adjustment prior to implementation but it is usually an indication of intent.

Thus it is not surprising that a few months after Parliament voted against changes to the GV program, the same proposal is now back on the table. Except much broader and more severe.

Why is this happening now?

The Golden Visa program has become (rightly or wrongly) associated with the “ills” that have affected the real estate market. Three factors stand out:

- Properties have become unaffordable to many local residents, in particular the younger generation

- With GV requiring such short stays, most properties have made their way to the short-term local lodging (AL) market that has displaced local residents and changed the characteristics of entire neighborhoods. As a result, the number of residential rentals has diminished

- The EU has been fighting against GV programs for some time, claiming they contribute to money laundering and possibly even to allowing the entry of terrorists into the Schengen area, and it might just be time to concede on this point

However, the government has not limited its proposals to the Golden Visa program.

A summary of the proposed changes

Much has been written about the proposed changes. For the moment, nothing is certain. The public consultation period runs for one month, to March 16th, 2023. Legislation could theoretically be implemented by decree. Even with resistance in parliament, the government has a majority, so can push changes through by itself.

The changes proposed include (the list is limited to those most likely to impact international investors and future residents):

- New real estate Golden Visas will no longer be allowed, of any type, anywhere

- Golden Visa renewals will come with conditions. Applicants and GV holders will be required to either make their property their primary residence or to ensure it is placed on the long-term rentals market. Those conditions are substantially different to the original conditions that were part of the GV program

- Incentives for transferring properties from short-term rental (local lodging or AL) to long-term rental (arrendamento)

- Compulsory rental of empty properties

- Rent control/caps

- The government will in some cases become the tenant with the right to sublease

- Penalties for planning delays

- Elimination of early repayment penalties on mortgage balances

Although a few positive measures have been proposed, they have been drowned out in the wave of uncertainty and by protests about the proposed changes. The general consensus from across almost all sectors of society, civil and professional, is that the government will never be able to implement all its proposals as some are not constitutional. I am neither a lawyer nor a constitutional expert, so I will simply point out the areas that appear to be most problematic:

- Appropriating vacant properties and forcing them onto the long-term lettings market

- Changing the terms under which original GV were granted, specifically in relation to the renewals. Most GV applicants chose the Portuguese GV program because of its low-stay requirements. Therefore, expecting that GV applicants make the property they have purchased (ignoring for the moment that some may not be suitable for permanent habitation) is unrealistic, and so the only option available under the proposed changes is to place the property on the long-term rental market

- Providing tax incentives for those moving from short to long-term lets, but excluding any rentals to immigrants (will an immigrant therefore be charged 25% more than a “local”, and indeed after how many months in the country, if ever, does an immigrant become “local” resident?)

- The government appointing itself as the tenant, with the right to sublet (a practice not common in Portugal) and with a government that is generally slow to pay

- Ongoing rent caps, contrary to the principle of an open market and freedom of use of private property

- Forcing Golden Visa investors to link renewals to a change in the use of their property to long-term rentals, in situations where the purchase is done in a project or condominium which is specifically zoned for tourism, for example, seems contradictory and difficult to implement given the legal classification of the property

The debate on social media, portals and discussion forums already includes threats by individuals or groups of individuals, to take the government to court if it proceeds with some of its proposals.

Practical steps that can be taken now

Among the uncertainty, most professionals and advisors are advising caution. That is fair, especially as a large part of the content of this article may change within weeks. However, there are some practical steps that appear sensible, low or relatively low risk, and that make the most of the changes. Some examples:

- Paying down mortgages: with increasing interest rates, anyone with capital in Portugal can reduce uncertainty and avoid early repayment fees, that have now been waived. For Portuguese citizens and residents who have some savings, do not have international investments, and are relying on paltry savings rates offered by local banks, the decision seems a “no-brainer” in most cases

- Switch on some utilities: to ensure that your property is not considered vacant, it seems as though the government will want to see evidence of some services being delivered within the previous 12 months

- Moving property into the long-term rental/letting market: generally, with the demand for long-term rental properties increasing due to residency visa programs such as the D7 (passive income or retirement) and D8 (digital nomad), and with the proposed special tax payable by AL owners, the proposed end of AL by 2030, and the tax exemption offered to those who move from AL to long-term rentals, there has never been a better time to start planning the move

- For existing GV investors, improving the chances of a Golden Visa renewal under new proposals: with the government progressively encouraging a move from short to long-term rentals, getting on a recognized long term lettings program is essential. A lot of people are talking about potential legal challenges if the government ploughs ahead with some of its proposals. But legal action can be time-consuming. Protecting income streams and asset value, together with guaranteeing residency, should be accomplished first.

Ignoring the history of policy-making in Portugal is risky. When a senior political figure makes an announcement or a prediction of this type, change is usually inevitable. It does not mean that the changes will be implemented exactly in the manner of the original announcement, but it is an early warning that changes will happen.

Most of the proposals are likely to be implemented, to a greater or lesser degree.

We observe government already providing some solutions to the challenges it has created with its own proposal. An example is the proposed 7-year tax exemption (until 2030) on income for owners who move from AL or local lodging, to arrendamento or long-term lets.

Based on past experience of other programs such as the NHR regime, that lasted 10 years at 0% tax before being changed, it is likely that within the 7 years the zero-tax position will erode. Acting swiftly to ensure a degree of certainty in a continuously changing fiscal landscape, is crucial. Also, expect many exceptions to the rule.

For new applicants, what is the alternative to the Golden Visa?

Portugal needs to attract more permanent residents who contribute directly to the local economy by spending on local services, and who pay their tax locally (by becoming tax residents).

Portugal has a residency visa known as the D7, for applicants with a passive income. Recently, digital nomads may apply for residency via the D8 visa.

The D7 and D8 visas are more flexible than the Golden Visa in that applicants can rent or buy a property. There are no geographic restrictions or minimum value. Conversely, applicants must live in the country for, on average, more than half a year, each year. The GV only requires an average of 7 days per annum.

Disclaimer: expect some of this to be outdated by the time it is published, and when seeking advice from duly qualified professionals on the changes, don’t rely on one single “expert” – consult or poll several!

The changing portuguese real estate market ( Part 3 )

Emerging sources of clients, supply versus demand imbalances and much more.

The chasm between cost and access to accommodation by local people, and the cost of delivering new inventory

In a report by CIA Landlord Insurance in the UK, published in March 2022, Lisbon is ranked as the third least viable city in the world in which to live, if you are renting. This is due to the discrepancy between disposable income for local people, and the cost of housing.

The Portuguese government has no consistent policy to deliver new housing, much less affordable housing, on any scale. Delivery of Build to Rent, previously also known as PRS (private rental sector), inventory, is practically impossible due to, among other factors, the tax burden. At least 35% of the total cost of any new construction is tax (of which the most significant are: VAT of 23% on cost of construction; 1.23% VAT on sales agency commission; around 5-6% IMT; notary costs; fees and contributions, including compensatory payments, by developers to municipalities). This excludes the cost of bureaucracy and delay which are borne by investors as a reduction in returns, and may be transferred to end buyers via price increases.

Why will new build continue to increase in value (and price)?

In addition to the benefits of newer, more efficient, more environmentally considerate technologies and materials, all of which come at a price, there is also the cost related to the process of developing a new project. As comment by a senior executive at a leading real estate consulting firm in Portugal: challenges include “high property taxes, VAT, and the sheer time it takes to get planning permission from city halls and local councils. This, in turn, makes it impossible for developers that normally plan ahead by up to 10 years, to keep to their original costings and budgets, thereby scaring off investors in this particular residential housing segment.”

The Portuguese Property Survey (PIPS), produced by the magazine Confidencial Imobiliário and the APPII, in May of 2022, reported that there had been an “increase in construction costs of 18% over the past year”. This cost will have to be passed on, in part or in full, to the end buyer.

A combination of existing lack of product, low levels of new build, an increase in labour and materials costs, high tax and slow planning cycles, mean that it is impossible to deliver affordable new build. Any new build that is perceived as cheap should immediately raise a red flag.

As most of the underlying causes of cost are structural and not easy to fix quickly, and consequently with new build prices expected to continue to rise, the Portuguese off-plan market presents an excellent opportunity for investors, both institutional and retail (end buyers). Residential developers willing to spend the time can benefit from uplift in land values when successfully taking a project through planning, and end buyers can benefit from higher-than-average ROI and ROC because of capital appreciation during the build cycle. This is sensible foresight based on sustained demand for end product, rather than the speculative type of investment that characterised the years prior to the financial crash of 2008-9.

The need for urgent change across the sector

The current inflationary cycle means that developers are naturally more risk-averse, as are buyers. In a conversation with a large real estate consulting company recently, I was surprised to hear an experienced executive imply that he expected developers to underwrite the risk of a volatile market so as to offer greater buyer protection. He seemed to fail to recognise the substantial risks already undertaken by developers, many of which are difficult to quantify to an end buyer without laying bare the hugely prejudicial environment in which developers operate in Portugal. The opinion also seemed to contradict the so-called “appeal” of Portugal. If a country is indeed such an attractive investment destination, then surely a more balanced approach between developer and buyer risk must be adopted?

The combination of factors (or challenges) outlined above, make it “impossible to create new build projects at affordable prices for Portugal’s lower-middle and middle classes.” As we have been arguing for some time, eon way to inject more affordable product into the Portuguese market, is to approve, develop and sell more expensive product such that a percentage of larger schemes can also deliver an affordable housing component. Many ways exist to do this, such as waiving VAT (or applying a reduced rate of VAT) on the affordable housing component of any development; encouraging developer-buyer shared ownership schemes by waiving IMI and offering reduced VAT on new build; or reducing IMT on new builds that meet certain environmental or other criteria, they have a secondary positive effect on helping to meet other government targets.

It is even possible for the government to link VAT to inflation in an inversely proportional ratio, such that VAT is capped at the moment of project approval, at the prevailing rate, but then falls in line with inflation as and when costs are incurred: the logic is that if costs go up then the government will still earn its tax as per the original estimate – after all, with no value whatsoever being received by the developer in exchange for VAT payments, it seems at best grotesque that the government should benefit while consumers and economic agents suffer. A similar situation exists in respect of fuel duty in Portugal, that could benefit from a similar inflation-linked VAT solution.

Ultimately, if the government is unwilling to sacrifice its tax revenue, then it must offer developers, who are taking most of the risk, incentives for them to build new product.

What is evident is that development models will have to change and for this to occur and the roles of the protagonists will have to be remapped. Some examples of the possible trickle-down effect:

- The government needs to reduce the tax burden on real estate development, starting with VAT

- Councils need to start adding more value, beyond simply having the power to approve projects and ask for contributions. The council must deliver value directly to the local community, in exchange for the revenue it receives from developers. The percentage of monies received from developers that is used for general municipal expenses should be capped, and the remaining amount ring-fenced for direct investment into the local area of the development

- Developers need to promote and build products with a client type in mind. Generic products with little focus or differentiation will slowly disappear

- Banks need to undertake project-based risk analysis, not cross-collateralisation. If a project does not stand on its own merit, it should be turned down. This means banks recruiting industry experts who understand sectorial context and end buyer behaviour, rather than just bricks and mortar

- Buyers will need to change their mind set from the transactional to the context-driven aspirational. Over time, mini “joint ventures” or collaborations with developers should be allowed to develop, creating a shared objective approach

- End user finance should become increasingly flexible – we are already starting to see some solutions emerge in this area

- Real estate agencies should improve efficiency, with technology less of a differentiator due to universal access. As a result, real estate companies should be able to reduce their operating costs and consequently drop their levels of commission, contributing to lower transaction costs. They should be able to change their remuneration model, moving away from the commission-only model, to paying (at least in part) base remuneration, improving levels of quality in the sector, greater job security and ultimately more sales (and therefore inward investment). This will be reflected in a greater level of certainty which is of huge importance to alleviating pressure on social care, healthcare and associated sectors

- The Manpower Group’s May 2022 talent shortage survey demonstrates that Portugal is the world’s second most difficult recruitment market, with 85% of companies reporting difficulties in filling positions. Given that there is an abundance of qualified and indeed talented human resources in Portugal, it is clear that matching supply to demand is as much an issue in the human resource space as it is in the real estate sector.

In the Algarve, employers who continue to promote heavily seasonal employment will soon need to factor in the higher accommodation costs during the summer. In particular, those companies attracting non-resident, seasonal resources will soon be forced to contribute to the cost of housing during the competitive peak season, failing which the remuneration may simply not be sufficient to allow seasonal labour to move for the short summer. These shortages are already being experienced in other markets with similar seasonal characteristics to the Algarve.

Conversely, employees and workers need to adapt their thinking to a challenging reality for all protagonists in the real estate sector. Those who are or wish to be real estate agents should be ready to commit to sales targets and to be measured on results. The mentality of real estate sales as a quick and easy way to make money, or for someone to turn to when desperate for a ”filler” job, must disappear. Likewise, for companies looking to work with talented individuals, basic aspects such as paying out of pocket business expenses and the payment of competitive commissions must form the basis for attracting new talent.

Bibliography

Building costs hamper development – Essential Business (essential-business.pt)

Casas para comprar mais caras — idealista/news

Oferta de casas à venda em Portugal desceu 25% num ano — idealista/news

Lisbon house price increases higher than London – Essential Business (essential-business.pt)

Best Places for Digital Nomads? Lisbon, Miami Attract High Earning Executives – Bloomberg

Americans Moving to Europe: Housing Prices and Strong Dollar Fuel Relocations – Bloomberg

Sale of homes to foreigners increases by more than 70% – Portugal Resident

Real Estate Speculation Has Made Lisbon One of the World’s Most Unlivable Cities (jacobin.com)

Home – CIA Landlord Insurance (cia-landlords.co.uk)

Portugal Will Be the First European Housing Bubble To Burst in 2023 – Value of Stocks

Preços das casas em Portugal cresceram 13,2% no segundo trimestre – Expresso

The changing portuguese real estate market ( Part 2 )

Emerging sources of clients, supply versus demand imbalances and much more.

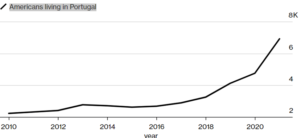

The increase in the presence and importance of the North American market

The Portuguese borders agency, SEF, has reported a large growth in US citizens choosing Portugal as their residence. While admittedly from a tiny base, the growth of this market underscores the increase in relative wealth of the average person seeking Portugal as their new home. Even those Americans who only receive Social Security payments, are receiving a pension substantially above the Portuguese average. The Canadian market is equally important, because a number of Canadians of Portuguese descent are seeking a return to their roots, and although the Canadian dollar does not represent the same purchasing power as the US dollar, incomes are substantially above those in Portugal. The USD and CAD have appreciated 20% and 14%, respectively, over the last year.

As Bloomberg reports, “retirees and the wealthy have traditionally been the prime buyers of real estate in Europe. But relatively cheap housing — particularly in smaller cities and towns — and the rise of remote work have made the continent alluring to a wider range of people, including those who are younger and find themselves priced out of the housing market at home. Growing crime rates in some US cities and political divisions have also led Americans to look across the pond for a quieter lifestyle, buoyed by a euro that just dropped to parity with the US dollar for the first time in more than 20 years.”

The effect of the supply and demand imbalance

Essential Business, in an article in July 2022, cites that the “residential segment, which today is highly dependent on real estate development (new build) is Portugal’s weak point at present, with the number of units absorbed by pre-existing products (second-hand) in the market far more expressive when compared to new products, owing to an absence of sufficient new stock in the market. The new build market has flatlined since 2011.”

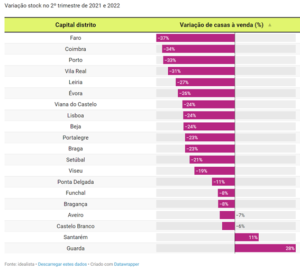

In an article, also in July 2022, published by the idealista portal, it is reported that there has been a 25% decrease in available inventory over the preceding 12 months. This problem is most acute in the Algarve problems, where supply has diminished 37% year on year.

Although rents have also gone up in value, they have not done so by the same margin as sales prices. For this reason, and despite the perception that rents have become expensive relative to 2010, they are still more competitively priced in 2022 than properties for sale.

The changing portuguese real estate market

EMERGING SOURCES OF CLIENTS, SUPPLY VERSUS DEMAND IMBALANCES AND MUCH MORE

The growing popularity of Portugal

Some would say that it is ironic that the international market and investment has done what Portugal and the Portuguese could not find the courage to do themselves, namely value their patrimony fairly. With decades of cheap real estate culminating in the financial crash of 2008-2009, the Portuguese were extremely hesitant in making investments in the real estate market of their own country. Accustomed to seeing the dramatic effects of global crises reflected in extremely difficult local market conditions, the majority of the population remained sceptical when the first signs of a recovery when noted around 2014. As international investment grew, bolstered by programmes such as the Golden visa and the non-habitual resident programme, real estate prices rapidly increased, and by the time most Portuguese had gathered enough courage to act, most had been priced out of the market.

The effect of Portugal’s popularity on real estate prices

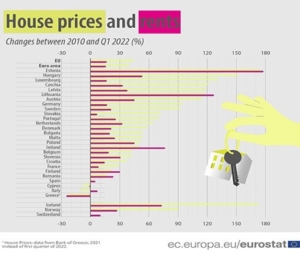

According to a report compiled by Idealista, Portugal prices have increased 70% in 10 years (2012-22), much higher than the European average of 45%.

The source of growth

As an example, Savills’ World Cities Prime Residential Index, which includes 30 cities around the world, ranked Lisbon as the 7th city where prices had grown the fastest in the first half of 2022, at 3.7%, versus an index average of 2.4%.

The role of foreign direct investment (FDI) on Portugal’s real estate market

Although the cyclical nature of real estate markets (and indeed economies) is acknowledged, this decade-plus cycle of sustained growth in Portugal, largely independently of a pandemic, a war and of somewhat depressed internal demand, seems to indicate something different. Given that Portugal’s internal market is largely unable to sustain such growth, due to still-low salary levels (and consequently limited disposable income) and small size, it is the international market and foreign investment that has been the main driver of this trend.

Backing up this opinion is a quote in Essential Business in July 2022 that confirms that “in 2012, as Portugal was still in the depths of the Great Recession, 46% of investment in Portugal came from overseas, today that figure has shot up to 85%…the overall investment in real estate development in Portugal, in 2016, was €200 million of which less than 50% came from overseas investors. That figure has shot up to an incredible €375 million in 2021, a year in which the world was still affected by the pandemic.”

The National Institute of statistics reports that investment from EU countries increased by 72.3% in Q1 2022, while foreigners buying from non-EU countries increased by 79.1%. In total, foreigners acquired 2556 properties in the first quarter of 2022.

At a granular level, what we observe is the increase in wealthier investors and buyers, meaning that competition for product is greater, prices tend to increase and demand for the upper and luxury segments of the market including new build, remains fairly buoyant.

One of the reasons for this is the trend described in the Henley global citizens report 2022 which shows that Portugal ranks in the top 10 countries expected to receive new millionaires during this year, approximately 1300. New World Wealth shows that Portugal 4, for example, has been one of the most popular destinations for the flow of HNW capital, capturing some of the 4500 high net worth South Africans that have left the country in the last decade.

Bloomberg UK also quotes a Savills report stating that Lisbon, together with Miami and Dubai, is ranked as the top city for high earning remote based talent, specifically senior staff.

Long-term rentals: The future of the rental market in Portugal?

LONG-TERM RENTALS:

THE FUTURE OF THE RENTAL MARKET IN PORTUGAL?

As recently as two years ago, it was unquestionable that Portugal provided Europe’s best investment destination. A growing economy, falling unemployment, a recovering real estate market, an investment surge in real estate driven primarily by the very successful Golden Visa program, a wave of (mostly) wealthy foreign retiree immigration driven by the Non Habitual Resident program, all this fuelled by 8 successive record-breaking years in the tourism industry, and no one could question the underlying fundamentals. Add to this the fact that Portugal had taken a long time to start to recover from the losses caused by the 2008-9 financial crisis, with property values falling as much as 40% in some locations.

The result of the perception of an improvement in the investment climate and the many measures intended to stimulate the economy was a jump in foreign investment. No sector felt the impact of this increase in capital inflows like the real estate market. From Chinese investors to French residents, the country’s real estate boomed and in 3 years, Lisbon had seen property growth of 60% and off-plan sales of modern, new-build product were back to full swing as if the recession had never happened.

Much of the growth was caused by investors who saw in Portugal not only an opportunity for capital appreciation from a low base, but also the possibility of rental yields. The country’s regulated, but very low tax, regime called the Alojamento Local, meant that early buyers who made their property available to the short-term rental market, were paying approximately 4% tax on gross revenues.

However, since then, we have observed the beginnings of dissatisfaction with over-tourism, the “expulsion” of local residents by (mostly) foreign owners, leading to a loss of character of entire neighbourhoods which were the drawcard attracting investors and visitors alike to the country’s authenticity, and an increased lack of respect for remaining local residents.

As a result, the government, which is in a parliamentary coalition with far-left parties, has set out a strategy of (not-so-gradual) assault on those perceived to be wealthy. And, unfortunately, as houses and apartments with sea views elicit a much more visceral response than pieces of paper known as shares or even a pile of intaglio paper known as money sitting in bank coffers, the government has set its sights firmly on financially penalising all those who own real estate.

While long-term rental contracts have historically paid capital gains tax (mais valias) on gross revenues, the government now appears to have the short-term rental market in its sights, especially if property is being managed as a short-term investment or let to the short-term or tourist market. There is talk that taxation may reduce for longer, more stable contracts, meaning that the discourse is that the short-term rental market may soon lose some of the many advantages it has, relative to longer contracts.

In 2017, the Portuguese government started its assault on real estate owners by approving the AIMI, an extraordinary real estate tax which applied to all owners who singly owned more than €600,000 of real estate (or €1,2 million as a couple). The law was named after the leader of Portugal’s extreme-left party, who campaigned tirelessly for its adoption.

Also in 2017, changes to the local lodging (Alojamento Local) legislation were implemented, including:

- An increase of the taxation basis from 15% to 35% of gross revenue, meaning an effective increase in the base rate of taxation on short-term rentals from less than 4% to around 10%. While still very competitive, the increase was significant

- Application of employer’s social security for companies managing client properties

- Higher water rates in some municipalities for properties registered as local lodging

- The need to present detailed calculations and proof of expenses, effectively eliminating the simplified regime for owners with annual rental values of around €27,000

It was also in this year that owners of local lodging establishments became aware that all of them had been caught by a little-known legislation which meant that anyone registering for short-term rentals was liable for capital gains. This remains an unclear and little-known aspect of the Alojamento Local.

In 2018, with a number of complaints about the effects of excessive tourism and short-term let properties, and the adoption of stricter rules in locations as diverse as Paris, Barcelona, New Zealand, Thailand, and Croatia, meant it was only a matter of time before the government started to change short-term rentals even further. New legislation, which has been approved by parliament and promulgated by the President, broadly forces the following changes:

- Municipalities will have the right to define zones with quotas on the number of short-term let properties, and owners will be limited to a maximum of 7 short-term rental properties within these zones

- Local lodging licences are personal and non-transferable in these areas and so if the property is sold, the new owner may not be able to get the licence renewed if the quota for that area has been reached. Buyers should be particularly careful about historical suburbs of Lisbon including Mouraria, Restelo and similar

- Condominiums will have the right to determine if and whether local lodging can be assigned to a property. Approval will require at least 50% of all voting members or owners

- Condominiums can charge a premium of up to 30% on condominium fees for those renting short-term

- Multi-risk and liability insurance is compulsory and must now also cover damage by clients to condominiums

- All client and tenant documentation must now be in three languages

These legislative changes will come into effect 60 days after their final approval in Parliament, forecast for October.

As a result of these changes, the market is starting to look more seriously at long-term rentals. Because long-term rentals, and even longer winter rentals of 8 months or more, are scarce (most owners prefer to make as much money as possible in the summer), Algarve Senior Living explains to customers how winter lets can complement summer revenue or substitute, in most cases, the summer revenue through an alternative model. Although online booking platforms have made direct marketing by owners much easier, and drastically reduced the role of the tour operator, many owners have yet to fill their properties fully beyond the peak months. It is important that owners do detailed calculations including expenses and tax, to determine which model works best for their propery/ies.

Algarve Senior Living has operated its unique model of long winter monthly lets, alongside the shorter summer weekly lets, for several years. Owners are now questioning whether they should consider transitioning to long lets if they currently operate summer lets only. We have seen an increase in the number of our property owners making their properties available for at least 6 months in the winter, in an attempt to balance the revenue streams in the summer and winter.

Advantages for owners of long-term and winter lets in their properties

- Winter lets are an excellent way to make extra revenue in months which are usually slow and where properties are closed

- Taxes and legislation surrounding short-term rentals are increasing, with more changes already approved by Parliament and the President set to become law by the end of 2018. Long-term rentals avoid these changes which affect the short-term lettings market

- There is already talk of a property and a real estate bubble impacting short-term rental values so owners can protect their assets by negotiating good long-term rental values while the market is still buoyant

- While the taxation is higher (28% versus around 10-16%, depending on VAT, for short lets), this difference is forecast to reduce as taxation on short lets increases

- Expenses, including cleaning, in long-term lets are paid by the tenant and not included in the rental

- Security deposits are higher, churn is lower

- Commissions from third parties may be lower. In the case of Algarve Senior Living, commission is added to the negotiated base rental amount

- Owners have time to vet and select their guests. Checking references is possible

- Long-term tenants tend to be seniors or families. There is less damage and properties benefit from year-round occupation

- For owners with Alojamento Local, 2018 is the year in which they can move their property from category B (Alojamento Local or local lodging) to category F (Arrendamento or long-term let) and suspend any capital gains which has been caused by the AL status. This is of particular relevance to any resident owners, such as Portuguese landlords, as CGT is much lower as a resident.

Advantages for tenants of a long-term rental

- Stability: knowing that they have a place to stay throughout the year, without the price fluctuations of the expensive summer months

- Visibility of expenses allowing for better planning

- Expenses are controlled directly by tenants, so if they wish to use more air conditioning or heating, they pay the bill, whereas if they decide to use blankets, they can save

- Contracts will allow those tenants who qualify, to apply for Portugal’s tax-free Non Habitual Resident status

Challenges for tenants of a long-term rentals

-

- Algarve Senior Living explains in detail the reason why tenants cannot expect to find quality property in good locations at discounted prices: in addition to the boom in demand, many tenants did not understand that long-term rentals are still taxed much higher than shorter rentals

- Many tenants looking for a long-term or annual rent, finding prices higher than they imagined, enter into a shorter contract in the slower winter months hoping they will then find something suitable when they are living locally. While this is sometimes the case, it often does not work for three reasons:

- The area selected is not necessarily the one in which they finally wish to settle. Their landlord has no knowledge of other areas nor any interest in finding a solution which will mean losing a winter rental earlier than planned

- There may be a special requirement, such as pets, which makes the list of available inventory very short indeed. Companies like Algarve Senior Living have spent years compiling their portfolio of properties which often involves months of negotiation with owners. Even then inventory changes but due to a larger variety, finding an alternative is usually possible

- Every winter month which passes brings us closer to the expensive summer months which in turn sees a decrease in inventory and an increase in price. Often owners, who in November are nervous when they see an empty winter in front of them, become much more confident by March when they see the approaching summer months

- The largest challenge for tenants is to understand that often sacrificing one or more criteria in order to get a full-year rental contract, is better than sacrificing the length of time in the hope of then finding the perfect solution later. Without exception, the latter approach is always more expensive.

Algarve Senior Living hopes to continue to play an active role in explaining the benefits of long lets to property owners, and implementing fair long-term rental pricing for tenants in the context of a booming market. Our investment in www.luz-living.com, the Algarve’s first coastal residential project for expatriate seniors, offering both apartments to purchase or for long lets, underscores our commitment to this model.